Alright, let’s grab a cuppa and talk about something that keeps many UK homeowners up at night:flood risk home insurance UK coverage. Here’s the thing: it’s not just about ticking a box on an application form anymore. The conversation around UK flood insurance has gotten, well, a little complicated. And what fascinates me is why it’s become so complex, and what those intricacies mean for you, the homeowner.

For years, many of us probably just assumed our standard home insurance would cover us for anything the weather threw our way. But with climate change making headlines and extreme weather events becoming less ‘extreme’ and more ‘regular,’ that assumption is, frankly, a bit naive. The deeper truth is, understanding your flood risk home insurance UK coverage isn’t just a good idea; it’s absolutely essential. It’s about knowing the hidden context, the implications, and the subtle shifts that could leave you high and dry (or, ironically, completely submerged) when you need protection most.

The Rising Tide | Why Flood Risk is Changing Across the UK

Let’s be honest, the weather feels different, doesn’t it? We’re seeing more intense rainfall, longer periods of wet weather, and consequently, a rising threat of flooding. This isn’t just anecdotal; it’s backed by science and the grim reality faced by communities year after year. This shift is drastically reshaping how insurers view UK properties and their vulnerability.

The Environment Agency regularly updates its flood maps, and what we’re seeing is an expansion of what were once considered safe zones into new, unexpected territories. This means that properties previously deemed low risk might now find themselves in high flood risk areas UK . It’s a dynamic situation, and your postcode, which might have been a beacon of safety a decade ago, could now be flagged. This re-evaluation by insurers isn’t arbitrary; it’s a direct response to tangible changes in our environment and the increased likelihood of costly flood damage . And that, my friend, is why your premiums might be creeping up, even if your local river hasn’t burst its banks yet.

Beyond the Brochure | Decoding Your Flood Risk Home Insurance Coverage

When you’re looking at your insurance policy , it’s easy to skim past the dense paragraphs. But when it comes to floods, those details are gold. A standard home insurance policy usually includes some form of flood cover, but the crucial part is understanding its limits, exclusions, and the dreaded ‘excess.’ I’ve seen countless cases where people assumed they were covered for ‘all eventualities,’ only to find out their policy had specific caveats.

For example, does your policy cover damage from burst pipes and river flooding? What about surface water flooding (often called ‘flash floods’)? These distinctions matter. The core of it comes down to understanding your policy wording . Some policies might differentiate between ‘escape of water’ (like a burst pipe) and ‘flood’ (natural water sources overflowing). Others might have specific limits on the payout for flood-related repairs or replacement of contents. It’s not just about having flood cover; it’s about having adequate flood cover for the specific risks your property faces. Don’t be afraid to call your insurer and ask them to walk you through the specifics – it’s far better to clarify now than to face a nasty surprise during a crisis.

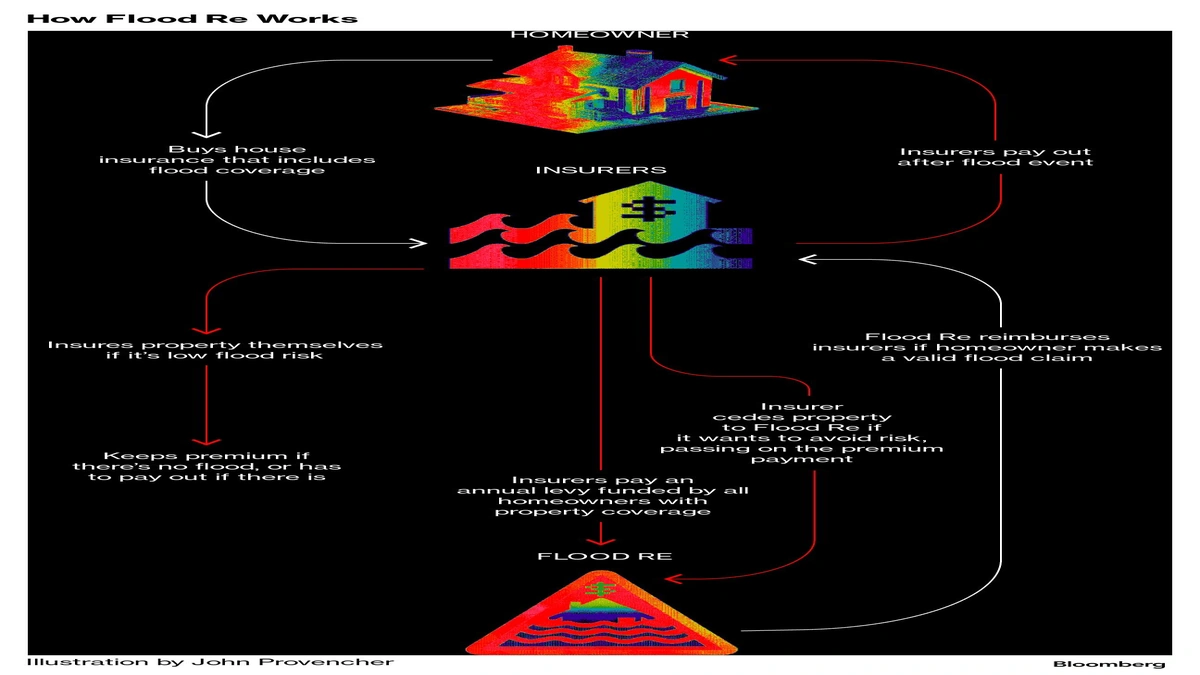

The Flood Re Scheme | A Lifeline, But Not a Silver Bullet

EnterFlood Re, a joint initiative between the UK government and insurers. It was launched in 2016 with a noble aim: to make the flood cover part of home insurance more affordable and accessible for properties in home insurance flood zones that were built before 2009. The ‘why’ behind Flood Re is powerful: to prevent a situation where vast swathes of the UK become uninsurable due to escalating flood risks.

Here’s how it works: when you buy home insurance, if your property qualifies, the insurer can pass the flood risk part of your policy to Flood Re. This means you pay a standard, affordable flood premium, and Flood Re takes on the financial risk of flood claims. Sounds great, right? And it is, for many. But it’s not a complete solution. It doesn’t cover businesses, properties built after 2009, or leasehold flats. More importantly, it’s a temporary scheme, set to transition out in 2039. This means homeowners need to use the breathing space it provides to invest inflood protectionand resilience measures for their homes. Relying solely on Flood Re without considering long-term solutions is like patching a leaky roof without ever fixing the underlying structural issue.

When Disaster Strikes (or Before It Does) | Navigating Claims and Future Coverage

Imagine the worst: your home has flooded. The immediate aftermath is chaos, but beyond the clean-up, there’s the long-term impact on your property insurance . If you’ve had insurance for properties with previous flood damage , you know it can be a tougher conversation with insurers. Some might increase your premiums, others might impose higher excesses, or in rare cases, even refuse cover if the risk is deemed too high and you haven’t taken mitigation steps. This is why proactive measures are so crucial.

Understanding your risk before an event allows you to take steps. This could involve installing flood barriers, raising electrical sockets, or laying water-resistant flooring. Many government flood schemes UK offer grants or advice to help homeowners implement these resilience measures. It’s an investment, yes, but one that can significantly reduce both the devastation of a flood and the future cost of flood insurance UK . Think of it like planning for your financial future with alow-cost term insurance plan– you hope you never need it, but you’re profoundly grateful if you do.

The True Cost | Why Flood Insurance Premiums Vary So Wildly

Have you ever wondered why your neighbour’s flood insurance premium is so different from yours, even if you live on the same street? It’s rarely straightforward. The cost of flood insurance UK is a complex calculation, influenced by a myriad of factors that go far beyond just your postcode. While living in a designated home insurance flood zone is a major contributor, insurers also look at the specific elevation of your property, the type of construction, whether you have a basement, and even the presence of local flood defences (and their maintenance status).

Your claims history, naturally, plays a significant role. Multiple past claims for flood damage will inevitably lead to higher premiums. However, insurers also consider the wider picture: regional flood data, climate change predictions, and the overall cost of potential repairs in your area. This is actuarial science at its most intricate, aiming to accurately price risk. It’s not about punishing homeowners, but about ensuring the system remains viable for everyone. That’s why being transparent with your insurer and taking steps to mitigate risk can sometimes lead to more favourable terms.

Ultimately, navigating the world of flood risk home insurance UK coverage requires a blend of vigilance, understanding, and proactive action. It’s not just about buying a policy; it’s about engaging with the evolving landscape of climate risk and ensuring your most valuable asset is genuinely protected. Don’t wait for the water to rise to start asking the hard questions.

Common Questions About UK Flood Insurance

What exactly does ‘flood risk’ mean for my home insurance?

For your home insurance, ‘flood risk’ refers to the likelihood of your property being damaged by water from natural sources like rivers, the sea, or heavy rainfall causing surface water to accumulate. Insurers assess this risk based on your location, property elevation, historical data, and proximity to water bodies.

Can I get insurance if my home has flooded before?

Yes, usually. While having insurance for properties with previous flood damage can make it more challenging, it’s often still possible. TheFlood Re scheme(for eligible properties built before 2009) helps. Insurers will also look at whether you’ve implemented any flood resilience measures since the last event.

How does the Flood Re scheme actually help?

The Flood Re scheme helps by making the flood insurance component of your home policy more affordable if your property is in a high flood risk area and was built before 2009. Insurers can pass the flood risk part of your policy to Flood Re, which then charges a fixed, lower premium for flood cover, making it accessible even in areas where it would otherwise be very expensive.

Are there things my policy won’t cover even if I have flood insurance?

Absolutely. Even with flood insurance, policies often have exclusions. These can include damage from burst pipes (often covered under ‘escape of water’ but with different terms), damage from groundwater seepage (unless explicitly covered), or damage if you haven’t taken reasonable steps to protect your property (e.g., leaving windows open during a storm). Always check your specific understanding your policy wording for exclusions and excesses.

What steps can I take to reduce my flood risk and potentially my premiums?

You can take several steps, including installing flood barriers, raising electrical sockets, using water-resistant materials for floors and walls, and ensuring proper drainage around your property. Participating in government flood schemes UK for mitigation advice or grants can also help. Informing your insurer of these measures might lead to reduced premiums or more favourable terms.