Alright, so you’ve got this brilliant idea, a fantastic team, and you’re ready to launch your startup in the UK. Exciting, right? But here’s the thing: amidst all the buzz of product development and market strategy, there’s a crucial, often overlooked, piece of the puzzle – startup business insurance UK. And let me tell you, it’s not just about ticking a box; it’s about safeguarding your dream, your livelihood, and your future. Many entrepreneurs, especially those new to the UK’s unique regulatory landscape, find themselves scratching their heads, wondering: “What do I really need?”

I’ve seen countless startups make common mistakes, from underinsuring to overlooking mandatory policies, only to face significant financial setbacks down the line. That’s why I’m here. Consider me your seasoned guide, helping you navigate the sometimes-confusing world of UK business insurance requirements with clarity and confidence. We’ll break it down, step by step, so you can focus on what you do best: building an incredible business.

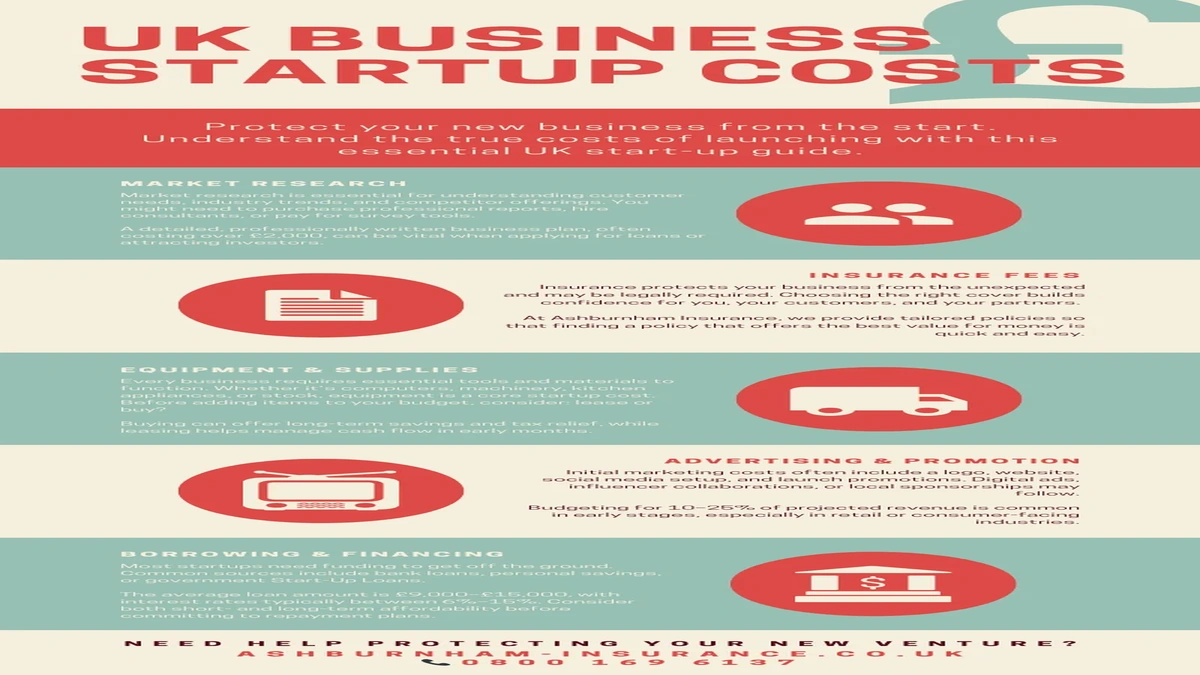

Why Bother? Understanding the UK’s Mandatory Insurance Landscape

Let’s be honest, insurance often feels like a necessary evil, another expense eating into your precious startup capital. But when it comes to the UK, some policies aren’t just good practice; they’re the law. Ignoring them isn’t just risky; it can land you in serious legal trouble and incur hefty fines. This is where understanding the `legal requirements for business insurance UK` becomes paramount.

The most prominent example, and a non-negotiable for almost any startup employing staff, is employers’ liability insurance. If you have even one employee – yes, even a part-timer or a remote worker – you are legally required to have this. It protects you against claims from employees who suffer injury or illness as a result of their work. The penalties for not having it are steep, up to £2,500 for every day you’re uninsured. That’s a quick way to derail a promising venture, isn’t it?

Beyond the legal mandates, there’s a whole spectrum of `types of business insurance UK` designed to protect your assets, reputation, and operational continuity. Think of it as building a robust safety net beneath your entrepreneurial tightrope act. It’s not just about compliance; it’s about resilience.

Decoding the Essentials | What Your Startup Really Needs

Okay, so we know `employers’ liability insurance UK` is crucial if you have staff. But what else should be on your radar? This is where it gets a little more nuanced, depending on your industry, your operations, and your risk exposure. Let’s delve into the core policies you’ll likely encounter and why they matter for your small business insurance UK strategy.

Employers’ Liability Insurance | The Unavoidable One

As we discussed, if you employ anyone, this is a must-have. It covers your legal liability for employee injuries or illnesses sustained during their employment. The minimum cover is £5 million, but most policies offer £10 million. You’ll typically receive a certificate of insurance, which you must display (physically or digitally) where employees can easily see it. It’s a fundamental pillar of responsible business operation in the UK.

Public Liability Insurance | For When Things Go Wrong Outdoors (or Indoors!)

This isn’t legally mandatory for most businesses, but it’s incredibly important. Public liability insurance protects your business if a member of the public (a client, a visitor, a passer-by) suffers an injury or property damage due to your business activities. Imagine a client tripping over a loose cable in your office, or your team accidentally damaging a customer’s property during an installation. Without this, you’re looking at potentially enormous legal fees and compensation payouts. Most businesses, especially those interacting with the public, offering services, or having a physical presence, should seriously consider this.

Professional Indemnity Insurance | Protecting Your Expertise

If your startup business insurance UK involves providing advice, design, or professional services (think consultants, designers, IT professionals, marketing agencies), then `professional indemnity insurance UK` is your guardian angel. It protects you against claims of negligence, errors, or omissions in the professional services you provide. Let’s say your advice leads to a client suffering a financial loss. This policy would cover your legal defence costs and any compensation awarded. It’s not legally required for all professions, but many professional bodies mandate it for their members, and savvy clients often insist on it.

Other Key Considerations for Your Commercial Insurance UK Portfolio

- Business Property & Contents Insurance: If you have an office, workshop, or even just valuable equipment at home, this covers loss or damage to your physical assets from events like fire, theft, or flood. It’s a good idea to consider your total asset value, including laptops, machinery, and stock.

- Cyber Insurance: In today’s digital world, a cyber-attack or data breach can be catastrophic. Cyber insurance helps cover the costs associated with data recovery, notification of affected parties, regulatory fines, and business interruption. It’s increasingly vital for almost every modern startup.

- Business Interruption Insurance: What if a fire or flood forces you to temporarily close your doors? This policy helps cover lost income and additional expenses while your business recovers, ensuring you can keep paying staff and bills.

Navigating the Market | How to Find the Right Policy Without the Headache

So, you’ve identified your potential needs. Now comes the task of actually getting the cover. The market for startup insurance UK can feel overwhelming, with countless providers and policy variations. Here’s my advice on how to approach it:

- Assess Your Risks Thoroughly: Before you even speak to an insurer, sit down and genuinely think about your business’s vulnerabilities. What could go wrong? What are your biggest exposures? This self-assessment is the foundation of getting appropriate cover.

- Compare Quotes, But Look Beyond Price: It’s tempting to go for the cheapest option, especially when every penny counts for a startup. However, ensure you’re comparing like-for-like. A cheaper policy might have significant exclusions or lower coverage limits. Use online comparison sites for initial quotes for `small business insurance UK`, but always read the fine print.

- Consider a Specialist Broker: For complex or niche businesses, a good insurance broker can be invaluable. They understand the market, can access policies not available directly, and can tailor packages to your specific needs. They can also explain what affects your `business insurance cost UK` and help you find competitive rates without compromising on cover. Think of them as your insurance translator and negotiator.

- Be Transparent: When applying for insurance, always provide accurate and complete information. Misleading an insurer, even unintentionally, can invalidate your policy when you need it most.

- Understand Your Policy: Don’t just file it away. Take the time to understand what’s covered, what’s excluded, your responsibilities, and the claims process. It’s like knowing how to use your car’s emergency brake – you hope you never need it, but you’re glad you know how if you do.

Common Pitfalls & Smart Moves for UK Startups

One common mistake I see entrepreneurs make is thinking theirpersonal car insuranceorhome insurancewill cover business activities. Let me be clear: it almost certainly won’t! Most personal policies have exclusions for business use. This is why dedicated commercial insurance UK is non-negotiable.

Another pitfall is underinsurance. You might think you’re saving money by opting for lower coverage limits, but if a major claim arises, you could be left with a significant shortfall. It’s a false economy. Regularly review your policies, especially as your business grows, takes on more staff, or expands its services. What was adequate when you were a sole trader might be completely insufficient six months later.

A smart move? Proactive risk management. Insurance is one layer of protection, but preventing incidents in the first place is even better. Implement strong health and safety protocols, robust data security measures, and clear operational guidelines. This not only reduces your chances of making a claim but can also positively influence your insurance premiums.

For more detailed official guidance on UK business insurance, you can always refer to reputable government resources, like theofficial UK government website on business insurance, which provides a good overview of the different types of cover.

Remember, your startup is your baby. You’ve poured your heart and soul into it. Investing in the right mandatory insurance UK isn’t an expense; it’s an investment in its survival and sustained growth. It provides peace of mind, allowing you to focus on innovation and expansion, knowing that you’re protected against unforeseen bumps in the road.

Frequently Asked Questions About Startup Business Insurance in the UK

Do I really need startup business insurance UK if I’m a sole trader?

While sole traders aren’t legally required to have employers’ liability insurance if they don’t employ anyone, other policies like public liability or professional indemnity are highly recommended. Your personal assets aren’t always separate from your business liabilities as a sole trader, making appropriate coverage even more critical.

What’s the difference between public liability insurance and professional indemnity?

Public liability covers claims for injury or property damage to third parties arising from your business operations. Professional indemnity covers claims for financial loss arising from your professional advice, design, or services due to negligence, errors, or omissions.

How much does UK business insurance typically cost for a new venture?

The cost varies wildly depending on your industry, number of employees, turnover, level of risk, and the specific policies you choose. A small, low-risk startup might pay a few hundred pounds a year, while a high-risk venture with many employees could pay thousands. Getting multiple quotes is key.

Can I get all my small business insurance policies from one provider?

Yes, many insurers offer comprehensive business insurance packages that combine several types of cover (e.g., public liability, contents, business interruption) into one policy, often at a more competitive price than buying them separately. It simplifies administration too.

What happens if I don’t have mandatory employers’ liability insurance?

If you employ staff and don’t have employers’ liability insurance, you could face fines of up to £2,500 for every day you are uninsured. Additionally, if an employee makes a successful claim against you for injury or illness, you would have to pay all legal costs and compensation yourself, which could be financially devastating for a startup.

Is cyber insurance truly necessary for a small startup?

Absolutely. Cyber threats don’t discriminate by business size. Even a small data breach can lead to significant financial and reputational damage. Cyber insurance helps mitigate these risks, covering costs like data recovery, legal fees, and regulatory fines, which can be crippling for a startup’s finances. It’s a vital component of modern business insurance requirements.

So, there you have it. Far from being a mere administrative hurdle, understanding and securing the right startup business insurance UK is a strategic move. It’s about building a foundation of security that allows your innovative ideas to truly flourish without the constant worry of unforeseen catastrophes. Get it right, and you’re not just protected; you’re empowered.