Ah, the freelance life! The freedom, the flexibility, the joy of being your own boss. It’s a dream for many, isn’t it? But then, reality often swoops in with a question mark, usually around things like, well, health insurance for freelancers USA cost . Let’s be honest, figuring out healthcare in the U.S. when you’re not part of a traditional employer-sponsored plan can feel like trying to solve a Rubik’s Cube blindfolded. It’s complex, it’s expensive, and frankly, it can be downright intimidating. But here’s the thing: it doesn’t have to be a mystery. I’m here to pull back the curtain and guide you through the maze, so you can focus on your passion, not your medical bills.

Many independent contractors and gig workers often delay looking into health coverage, hoping for the best. I’ve seen it time and again. The fear of the unknown, especially the potential cost, can be paralyzing. But ignoring it is never the answer. The goal here isn’t just to tell you what things cost; it’s to empower you with the knowledge to make informed decisions about your well-being and your wallet. We’ll dive deep into findinginsurance policy comparisonaspects for your unique situation, even if one of the tools is for a different region, the principle of comparison remains key.

Decoding the Jargon | Premiums, Deductibles, and Beyond

Before we even talk numbers, let’s get on the same page about the lingo. Healthcare in the U.S. has its own vocabulary, and understanding it is half the battle when assessing health insurance for freelancers USA cost . You’ll hear terms like `premium`, `deductible`, and `out-of-pocket maximum` thrown around, and they’re crucial.

- Premium: This is the most straightforward. It’s your monthly payment to the insurance company. Think of it like a subscription fee. You pay it whether you use the insurance or not. This is a big part of your immediate `health insurance options for freelancers` budget.

- Deductible: Now, this is where it gets a bit trickier. Your deductible is the amount you have to pay for covered healthcare services before your insurance company starts to pay. For example, if your deductible is $5,000, you’ll pay the first $5,000 in medical costs out of your own pocket each year before your insurer chips in. High-deductible plans often have lower premiums, which might seem appealing initially, but require a significant emergency fund. Understanding your `deductible and premium` balance is vital.

- Copayment (Copay): A fixed amount you pay for a covered health service after you’ve met your deductible. Visiting a doctor for a routine check-up might be a $30 copay, for instance.

- Coinsurance: This is your share of the cost of a healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service. You pay coinsurance after you’ve met your deductible.

- Out-of-Pocket Maximum: This is your financial safety net. It’s the most you’ll have to pay for covered services in a plan year. Once you hit this limit, your insurance company pays 100% of the costs for covered benefits. This includes deductibles, copayments, and coinsurance. It’s a crucial figure to know, especially for those worried about catastrophic medical events. This is a key component of the overall `out-of-pocket maximum` consideration for `self-employed health insurance`.

The interplay of these factors determines your total financial exposure. A lower premium usually means a higher deductible and potentially higher out-of-pocket maximums. It’s a balancing act, and what works best for one freelancer might not work for another. It truly depends on your health, your risk tolerance, and your financial situation.

Your Options | Navigating the Health Insurance Landscape

Okay, so you know the terms. Now, where do you actually get health insurance for freelancers USA cost that makes sense? You’ve got a few main avenues, each with its own quirks and advantages.

The ACA Marketplace (Healthcare.gov)

This is often the first stop for many `self-employed health insurance USA` seekers. The Affordable Care Act (ACA) marketplace, or Healthcare.gov, offers a range of plans (Bronze, Silver, Gold, Platinum) and, critically, potential subsidies. These subsidies come in the form of `tax credits for health insurance` that can significantly lower your monthly premiums, making `affordable health insurance` a reality for many.

Here’s the magic of the `ACA marketplace`: Your eligibility for these premium tax credits is based on your estimated household income. As a freelancer, your income might fluctuate, so it’s important to estimate carefully. The government wants to make sure healthcare is accessible, and these credits are a huge help. You can also get cost-sharing reductions on Silver plans, which lower your deductible, copayments, and coinsurance if your income is below a certain threshold. This is often the `best health plans for independent contractors` option for those who qualify for assistance.

Directly from an Insurer

You can always go directly to an insurance company like Blue Cross Blue Shield, UnitedHealthcare, or Aetna. They offer plans outside the marketplace. However, if you buy directly, you generally won’t be eligible for the premium tax credits or cost-sharing reductions that are available only through the marketplace. So, for most freelancers looking for cost-effectiveness, the marketplace is usually the better bet unless you don’t qualify for subsidies and find a better deal directly.

Short-Term Health Plans

These are exactly what they sound like: `short-term health plans` designed to cover you for a limited period, usually up to 12 months, with options to renew. They come with significantly lower premiums, which can be very tempting when you’re looking at the raw health insurance for freelancers USA cost . But here’s the catch (and it’s a big one): they don’t have to comply with ACA rules. This means they can deny coverage for pre-existing conditions, don’t cover essential health benefits like maternity care or mental health, and often have high out-of-pocket costs.

My take? Treat `short-term health plans` as a bridge, not a destination. They’re okay if you’re between jobs or waiting for open enrollment, but they offer far less comprehensive protection than an ACA-compliant plan. It’s a gamble, and personally, I’d rather not gamble with my health.

Professional Organizations & Co-ops

Sometimes, your professional association or a freelancer co-op might offer group health plans. These can be a fantastic way to access `health insurance options for freelancers` that might otherwise be out of reach. Organizations like the Freelancers Union, for example, have offered health insurance options in the past (though availability can vary by state). It’s always worth checking if your specific industry or guild has such benefits. The collective bargaining power can sometimes lead to better rates.

The Real Cost | What to Expect and How to Save

So, what’s the actual dollar amount you’re looking at for health insurance for freelancers USA cost ? This is where it gets highly individualized. Many factors play into it:

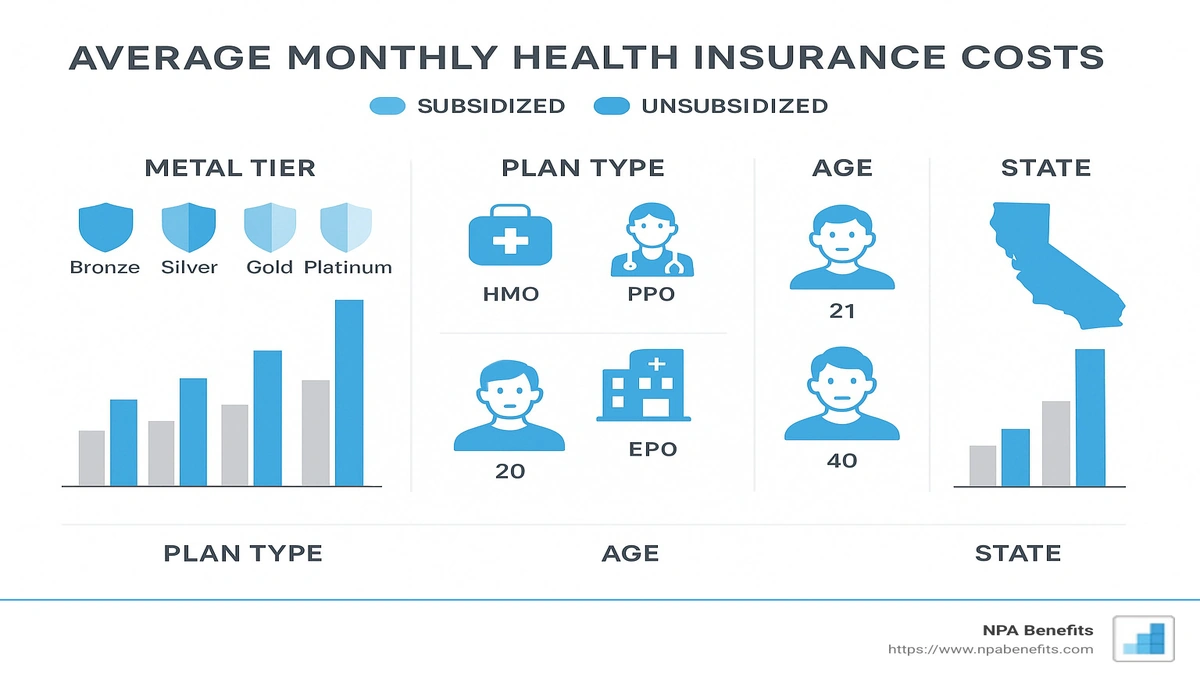

- Age: Generally, the older you are, the higher your premium.

- Location: Healthcare costs vary wildly by state and even by county. Urban areas might have more options, but also higher prices.

- Smoking Status: Smokers often pay significantly more.

- Plan Type: As we discussed, Bronze plans are cheapest but have high deductibles. Platinum plans are most expensive but cover more upfront.

- Income: Crucial for determining your `tax credits for health insurance` on the ACA marketplace.

According to Healthcare.gov, in 2024, the average unsubsidized premium for a 40-year-old on a Silver plan was around $500-$600 per month, but with subsidies, many people pay much less. Some even pay as little as $10-$50 per month after subsidies. This really highlights the importance of checking your eligibility for financial assistance.

Strategies to Lower Your Costs |

- Maximize Marketplace Subsidies: Seriously, don’t skip this step. Use the official Healthcare.gov website to see what you qualify for. Even if you think your income is too high, check anyway.

- Consider a High-Deductible Health Plan (HDHP) with an HSA: If you’re generally healthy and can afford the higher deductible, an HDHP combined with a Health Savings Account (HSA) can be a powerful tool. HSAs allow you to save money tax-free for medical expenses, and the funds roll over year after year. It’s a great way for `understanding healthcare costs for gig workers` while also saving for the future.

- Shop Around Annually: Plans and prices change every year. Don’t just auto-renew! Use the open enrollment period to compare different `health insurance marketplace for self-employed` options. A plan that was great last year might not be the `best health plans for independent contractors` this year.

- Negotiate Medical Bills: If you end up with a large bill, don’t be afraid to call the provider and negotiate. Many hospitals offer discounts for prompt payment or if you pay cash.

Making the Smart Choice | Tips from an “Insider”

Having navigated the insurance world for years, here’s my personal advice on selecting the right `self-employed health insurance` plan:

First, be brutally honest with yourself about your health needs. Do you have chronic conditions? Do you visit specialists regularly? Or are you generally healthy and only need catastrophic coverage? Your answers will guide you toward a plan that truly fits. A low premium might look great on paper, but if you’re constantly hitting a high deductible, it might not be the most economical choice in the long run. Sometimes, paying a bit more upfront for a lower deductible actually saves you money. Think of it like comparing alife insurance premium calculator– you’re trying to balance current cost with future benefit.

Second, always check the provider network. What good is a great plan if your favorite doctor isn’t in-network? This is a common pitfall. Make sure your preferred physicians, hospitals, and pharmacies are covered before you commit. Out-of-network costs can skyrocket and quickly derail your budget, completely changing your expected health insurance for freelancers USA cost .

Finally, don’t be afraid to ask for help. Navigators are available through Healthcare.gov (or your state’s marketplace) to provide free, unbiased assistance in understanding your options and enrolling in a plan. They’re literally there to demystify the process for you. Take advantage of their expertise!

The journey to finding the right health insurance for freelancers USA cost and coverage can feel overwhelming, but remember, you’re not alone. By understanding the core concepts, exploring your options on the marketplace, and being proactive about your choices, you can secure the peace of mind that comes with knowing you’re covered. It’s an investment in yourself, your business, and your future. So take a deep breath, and let’s get you covered!

Frequently Asked Questions About Freelancer Health Insurance

What is the average health insurance for freelancers USA cost?

The average unsubsidized premium for a 40-year-old on a Silver plan can be around $500-$600 per month. However, many freelancers qualify for significant subsidies through the ACA marketplace, which can reduce monthly premiums to $10-$150 or even less, depending on income and location.

Can I get a subsidy for health insurance as a freelancer?

Yes, absolutely! If your income falls within certain guidelines, you can qualify for premium tax credits (subsidies) through the ACA marketplace (Healthcare.gov). These credits can drastically lower your monthly premium, making `affordable health insurance` much more accessible.

What are my options if I have a pre-existing condition?

Under the Affordable Care Act (ACA), all plans sold on the marketplace (and most plans sold directly by insurers) cannot deny you coverage or charge you more because of a pre-existing condition. This is a major protection for freelancers. Short-term health plans, however, may deny coverage for pre-existing conditions.

Should I choose a high-deductible plan?

A high-deductible health plan (HDHP) can be a good option if you are generally healthy, don’t anticipate frequent medical visits, and have savings to cover the deductible if an unexpected health issue arises. HDHPs often come with lower monthly premiums and can be paired with a Health Savings Account (HSA) for tax-advantaged savings.

How do I enroll in health insurance as a self-employed individual?

The primary way to enroll is through the ACA marketplace at Healthcare.gov during the annual Open Enrollment Period (typically November 1st to January 15th). You may also qualify for a Special Enrollment Period if you experience certain life events, like moving, getting married, or having a child. You can also explore direct plans from insurers or professional organizations.

What’s the difference between PPO and HMO plans?

HMO (Health Maintenance Organization) plans usually require you to choose a primary care physician (PCP) and get referrals to see specialists. They typically have lower premiums. PPO (Preferred Provider Organization) plans offer more flexibility, allowing you to see specialists without a referral and often covering out-of-network care (though at a higher cost). Your choice impacts your `out-of-pocket maximum` and overall flexibility.